Key Personal Taxes and Potential Advantages for UK Non-Doms

A number of countries offer ‘remittance basis of taxation’ regimes to attract wealthy individuals to re-locate from other countries, such as Russia. These individuals are known as ‘non-doms’. Very simply expressed a non-dom is an individual not living in his/her country of ‘origin’.

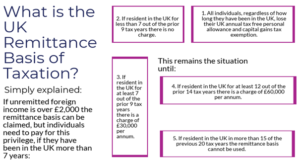

The UK remittance regime is a particularly attractive example and although the rules have changed since 2008, with the latest changes being implemented in April 2017, this regime remains of significant benefit to HNW non-doms living in the UK. In fact, the advantages for individuals living in the UK for less than 7 years remain very generous (please see below).

The UK remittance regime is a particularly attractive example and although the rules have changed since 2008, with the latest changes being implemented in April 2017, this regime remains of significant benefit to HNW non-doms living in the UK. In fact, the advantages for individuals living in the UK for less than 7 years remain very generous (please see below).

The rules are relatively complicated and you are advised to seek specialist advice, at an early stage, from a firm such as Dixcart, with expertise in this area.

Advantages Available Through Use of the UK Remittance Basis Of Taxation

- The remittance basis of taxation allows UK resident non-UK domiciliaries, who retain funds outside of the UK, to avoid being taxed in the UK on the gains and income that arise from these funds. This is as long as the income and gains are not brought into or remitted to the UK. Such individuals are only subject to tax on UK source income and gains.

Exceptions to the Remittance Rules

- Under an exception introduced in April 2012, no tax charge arises on remittances to purchase certain UK investments (these include the purchase of an interest in a commercial property business).

In addition, there are other exceptions, please contact Dixcart if you require further details.

Temporary Non-Residence in the UK

Non-UK domiciliaries who have unremitted foreign income and gains, and who cease to be resident in the UK, need to leave the UK and be non-resident for at least 6 complete years, if they wish to use the non-UK income and gains, that they held prior to becoming non-resident, to fund UK expenditure during their absence from the UK.

UK Inheritance Tax (IHT)

The UK IHT rate is 40% of the value of assets held (above a nil-rate band, which varies depending on circumstances).

- Non-UK dom individuals can benefit from only being subject to UK IHT on UK assets.

- However, this UK tax benefit does not last forever. The IHT position is typically affected, at the start of the 16th year of residence in the UK and then covers worldwide assets, not just those in the UK.

Additional Information

This is an extremely brief review of the UK remittance basis of taxation and UK IHT. These are complex areas and professional advice should be taken.

If you require additional information on this topic, please speak to Paul Webb or Peter Robertson at the Dixcart office in the UK: advice.uk@dixcart.com