A Guernsey ‘Qualifying’ Private Investor Fund (PIF)

Following consultation with industry in 2020, the Guernsey Financial Services Commission (GFSC) has updated its Private Investment Fund Regime, to expand the available PIF options. The new rules became effective on 22 April 2021, and immediately replaced the previous Private Investment Fund Rules, 2016.

Route 2 – the Qualifying Private Investor (QPI), PIF

This is a new route that does not require a GFSC Licensed Manager.

This route, compared to the traditional route, offers reduced operational and governance costs, whilst retaining substance within the PIF through the proper operation of the board and the close, on-going role of the Guernsey appointed licensed Administrator.

The Criteria

A Route 2 PIF must fulfil the following criteria:

All investors must meet the definition of a Qualifying Private Investor as defined in the Private Investment Fund Rules and Guidance (1), 2021. In this case the definition includes the ability to;

evaluate the risks and strategy for investing in the PIF;

bear the consequences of investment in the PIF; and

bear any loss arising from the investment

No more than 50 legal or natural persons holding an ultimate economic interest in the PIF;

The number of offers of units for subscription, sale or exchange does not exceed 200;

The fund must have a designated Guernsey resident and Licensed Administrator appointed;

As part of the PIF application, the PIF Administrator must provide the GFSC with a declaration that effective procedures are in place to ensure restriction of the scheme to QPIs; and

Investors receive a disclosure statement in the format prescribed by the GFSC.

Who Will the Route 2 PIF be Attractive To?

The Route 2 PIF will be particularly attractive to a range of Promoters and Managers as it reduces the overall formation and on-going costs of the PIF, whilst affording an appropriate level of regulation in the highly favoured jurisdiction of Guernsey.

This route allows a PIF to become self-managed (which is likely to further reduce costs) but still allows the flexibility of appointing a Manager if desired.

This route is suitable for investment managers, family office, or groups of individuals to develop a track record of investment management

The GFSC has noted that the new PIF rules do not widen or alter the definition of ‘collective investment scheme’.

Dixcart and Additional Information

Dixcart is licensed under the Protection of Investors (Bailiwick of Guernsey) Law 1987 to offer PIF administration services, and holds a full fiduciary license granted by the Guernsey Financial Services Commission.

The Guernsey Financial Services Commission (GFSC) has updated the Private Investment Fund Rules, to offer three alternate PIF routes, effective from 22 April 2021.

The new PIF options follow on from a GFSC consultation with industry in 2020, and in addition to the existing Protection of Investors (POI) Licensed PIF (Route 1), add two new options – the Qualifying Private Investor PIF (Route 2) and the Family Relationship PIF (Route 3).

The Three Guernsey Routes

Route 1 – the POI Licensed Manager PIF is the original PIF model whose criteria is; fewer than 50 investors (although no limit on the number of potential investors who can be marketed to), limits on investors in and out in a 12 month period, and, must have a Guernsey resident POI Licensed Manager appointed.

Route 2 – the Qualifying Private Investor (QPI) PIF is a new route which does not require a GFSC licensed Manager and is aimed at investors who meet the criteria of being a QPI i.e. able to evaluate the risks and bear the consequences of the investment. The Guernsey resident licensed designated Administrator of a QPI PIF is required, as part of the application process, to declare to the GFSC that it has effective procedures in place to ensure the fund is restricted to sophisticated investors only.

Route 3 – the Family Relationship PIF is the second new route that does not require a GFSC Licensed Manager. This route allows for the creation of a bespoke private wealth structure as a fund and requires a family relationship between investors. This route is only open to investors who either share a family relationship or who are an ‘eligible employee’ of the family and meet the criteria of being a QPI.

Interesting Features – Applicable to All Three Routes

Points common to all three routes are:

a one business day turnaround at the GFSC for the PIF applications;

no requirements for private placement memorandum (PPM) or other information particulars, although it is common for a PPM style document to be provided to potential investors;

can be closed-ended or open-ended;

must be audited; and

conflict of interest requirements apply to the directors managing the PIF.

Dixcart and Additional Information

Dixcart is licensed under the Protection of Investors (Bailiwick of Guernsey) Law 1987 to offer PIF administration services and also holds a full fiduciary license granted by the Guernsey Financial Services Commission.

For further information on wealth, estate and succession planning and the establishment and administration of a private investment fund, please contact Steve de Jersey at advice.guernsey@dixcart.com

Exempt Funds are an often-overlooked vehicle that could provide a client with a cost effective, tailored solution for meeting their long-term financial objectives.

Under an Isle of Man Exempt Fund regulatory requirements need to be met, however ‘Functionaries’ (such as the managers and/or administrators), have a lot of flexibility and freedom to achieve the fund’s purpose.

As a Functionary, Dixcart can assist professional service providers such as Financial Advisers, Solicitors, Accountants etc. in establishing Exempt Funds domiciled in the Isle of Man.

In this article, we will cover the following topics to provide a quick overview:

As the name might suggest, an Isle of Man Exempt Fund is established in the Isle of Man; therefore, Manx law and regulation apply.

All Isle of Man funds, including Exempt Funds, must conform to the meanings defined within the Collective Investment Scheme Act 2008 (CISA 2008) and regulated under the Financial Services Act 2008.

Under Schedule 3 of CISA, an Exempt Fund must meet the following criteria:

The Exempt Fund to have no more than 49 participants; and

The fund is not to be publicly promoted; and

The scheme must be (a) a Unit Trust governed by laws of the Isle of Man, (b) an Open Ended Investment Company (OEIC) formed or incorporated under the Isle of Man Companies Acts 1931-2004 or Companies Act 2006, or (c) a Limited Partnership that complies with Part II of the Partnership Act 1909, or (d) such other description of a scheme as is prescribed.

The limitations on what is not considered a Collective Investment Scheme are contained within CISA (Definition) Order 2017, and these apply to an Exempt Fund. Modifications to the rules outlined within CISA 2008 are allowable, but only on application and approval from the Isle of Man Financial Services Authority (FSA).

Appointing an administrator of an Isle of Man Exempt Fund

A Functionary of an Exempt Fund, such as Dixcart, must also hold the appropriate license with the FSA. Management and administration of Exempt Funds fall under Class 3(11) and 3(12) of the Financial Services Act 2008’s Regulated Activities Order 2011.

The Exempt Fund must meet the compliance requirements of the Isle of Man (e.g. AML/CFT). As an acting Functionary, Dixcart is well placed to guide and assist on all applicable regulatory matters.

Available asset classes for an Isle of Man Exempt Fund

Once established, there are no restrictions on the asset classes, trading strategy or leverage of the Exempt Fund – providing a large degree of freedom for achieving the client’s desired objectives.

An Exempt Scheme is not required to appoint a custodian or have its financial statements audited. The fund is free to implement whatever arrangements are appropriate for holding its assets, whether through the use of a third party, direct ownership or via special purpose vehicles to segregate separate asset classes.

Why establish an Exempt Fund on the Isle of Man?

The Isle of Man is a self-governing Crown Dependency with a Moody’s Aa3 Stable rating. The Manx Government boasts strong relationships with the OECD, IMF and FATF; working together with the local Financial Services Authority (FSA) and service providers to ensure a global and modern approach to compliance.

The business friendly Government, beneficial tax regime and ‘whitelist’ status make the Island a leading international financial centre with a lot to offer inbound investors.

Headline applicable rates of tax include:

0% Corporate Tax

0% Capital Gains Tax

0% Inheritance Tax

0% Withholding Tax on Dividends

What holding structures are appropriate for establishing an Isle of Man Exempt Fund?

Whilst CISA 2008 provides a list of applicable structures, ‘Open Ended Investment Companies’ (OEICs), and ‘Limited Partnerships’ are the most commonly used.

The use of a company, or a Limited Partnership offers a number of distinctive features, with only the general characteristics being presented below. For more information, relevant to your client’s specific circumstances, please get in touch.

Using an OEIC Structure for an Isle of Man Exempt Fund

An Isle of Man company benefits from a 0% tax rate on trading and investment income. They are also able to register for VAT, and businesses in the Isle of Man fall under the UK’s VAT regime.

There are no prescriptive requirements regarding the composition of a board of directors or the Exempt Fund documentation. It is however advisable, for the benefit of the investor, to include as much detail regarding the purpose and objectives of the Fund, in so far as a reasonable person might expect, to make a well-informed decision.

An OEIC can be established by the incorporation of a company under either the Companies Acts 1931, or the Companies Act 2006; the outcome of either vehicle will be comparable, but in some areas the legal form and constitution are quite distinct. Dixcart can assist with the effective establishment and administration of an OEIC holding structure for an Exempt Fund domiciled in the Isle of Man.

Using a Limited Partnership for an Isle of Man Exempt Fund

The Limited Partnership entity is a category of ‘Closed-ended Collective Investment Scheme’. The Limited Partnership will be registered under the Partnership Act 1909, which provides the legal framework and requirements of the vehicle, such as:

s47(2)

Must have one or more General Partners, who are liable for all debts and obligations of the firm.; and

One or more persons called Limited Partners, who shall not be liable beyond the amount contributed.

s48

s48(1) Every limited partnership must be registered in accordance with the 1909 Act;

s48A(2) Every limited partnership shall maintain a place of business in the Isle of Man;

s48A(2) Every limited partnership shall appoint one or more persons resident in the Isle of Man, authorised to accept service of any process or documents on behalf of the partnership.

Many of the services required for the establishment of a Limited Partnership on the Isle of Man can be provided by Dixcart. These include those relating to; General Partners, the registered place of business and the administration of the Limited Partnership.

The General Partner must be responsible for the day-to-day decision-making and management of the Partnership. However, the Partnership can engage third party intermediaries for advice and management services with respect to the assets.

Investment is typically made by way of an interest-free loan that is repaid on maturity, along with any remaining balance by way of growth, to the Limited Partners. The exact form that this takes will be determined by the terms of the Partnership and the personal tax circumstances of each specific Limited Partner. Limited Partners will be subject to the tax regime in which they are resident.

A working example of a Isle of Man Exempt Fund

Key Benefits of an Isle of Man Exempt Scheme Summarised

Simplicity of ownership – consolidates assets of any class into one vehicle with reduced administration for the Client.

Flexibility of asset class and investment strategy.

Cost efficiency.

The Client can retain a degree of control and can be appointed as a fund adviser.

Privacy and confidentiality.

The Fund administrator/manager is responsible for compliance and to meet the regulatory obligations.

The Isle of Man holds an Aa3 Stable Moody’s rating, has strong international relationships and is highly regarded as a jurisdiction.

Get in touch

Exempt Funds are outside the scope of normal fund regulation in the Isle of Man, and with the variety of holding structures available, this category of Fund is particularly suited for private investment.

Dixcart provide a single point of contact for the setup and management of Exempt Funds and Fund vehicle; establishing the fund and organising the formation and management of the underlying holding companies.

If you require further information regarding Isle of Man Exempt Funds or any of the vehicles discussed, please feel free to get in touch with Paul Harvey, at Dixcart Isle of Man, to see how they can be used to meet your objectives:

Dixcart Management (IOM) Limited is Licensed by the Isle of Man Financial Services Authority***

***This information is provided as guidance as at 01/03/21 and should not be considered advice. The most appropriate vehicle is determined by individual client needs and specific advice should be sought.

Guernsey is a leading domicile for funds, with more than 50 years of experience in the formation, administration and cross-border distribution of investment funds. It also offers a ‘lighter touch’ approach to Private Investment Structures (‘PS’), also known as Private Funds (‘PFs’), which are ‘related party’ investment structures, particularly suitable for family office arrangements.

Private Funds are of particular interest as platforms for wealthy families and small groups of “club” investors to hold a wide variety of assets.

Private Funds are bespoke structures with minimal or no fund regulatory status. There is no legal definition for a PF, and they can be a legal entity with a similar choice of structure; for example, a limited company, limited partnership, trust and/or a cellular company.

Why are Private Fund Structures of so Much Current Interest?

There are several reasons for the current, increased interest in PFs, including:

The ability for families and club investors to pool their assets and seek enhanced investment opportunities and greater economies of scale.

The ability to ‘unitise’ specific assets to facilitate joint ownership, e.g. an aircraft, paintings, real estate etc.

Independent calculation of the Net Asset Value (“NAV”) and external audit of a PF, if required, provides reassurance to investors.

A PF may offer a more straightforward concept for some clients, compared to trusts – particularly for clients in civil law countries.

The opportunity to undertake basic succession planning, where interests can be gifted to other family members over time.

A vehicle to hold a new business venture – with the ability to “lock in” investors, providing certainty and long-term commitment between them.

They offer a single platform for family offices to manage wealth – with the ability to hold higher-risk assets (which might otherwise cause fiduciary risk concerns for trustees with duties to beneficiaries).

A PF can also offer potential tax benefits, depending on the investors’ country(s) of tax residence.

Regulatory Position

The regulatory regimes of different international financial centres vary extensively and in Guernsey PFs are not subject to collective investment scheme legislation, as long as the following criteria are met:

there is a small, defined and closely-linked group of investors;

the investors are “sophisticated” by definition of their wealth and/or expertise;

the “spread of assets” (number of holdings in the PF) is limited.

Meeting the above criteria generally means that a PF is considered to be a fiduciary structure, rather than a regulated fund entity. As such, it will only be subject to light or to no fund regulatory requirements in Guernsey.

If the number of investors and spread of assets grows and exceeds Guernsey exemption rules or practice, regulatory consent is likely to then be required. Consent from the Regulator may also be needed in relation to the entity undertaking investment decisions.

EXAMPLES OF PRIVATE FUND STRUCTURES

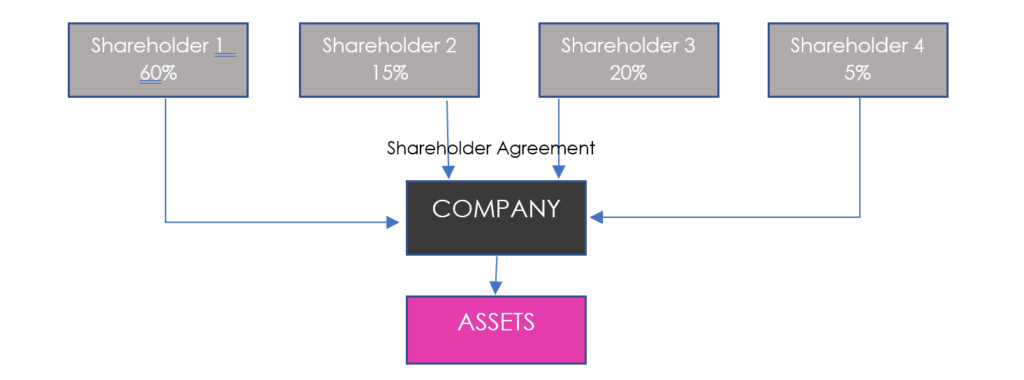

Limited Liability Company

The most straightforward structure is probably a Limited Liability Company with a robust shareholder agreement. The management and administration of the investment vehicle would be undertaken by a regulated Trust company with an option to outsource specialist management of more unusual assets to third party providers.

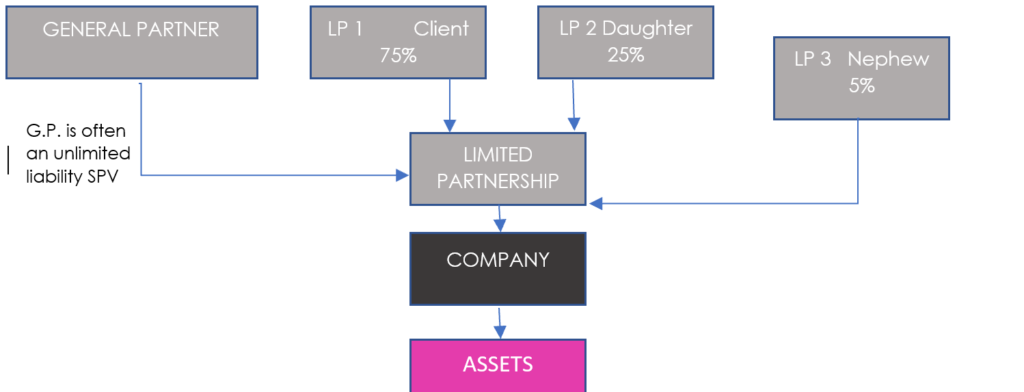

Limited Partnership

In this structure, a General Partner (‘GP’) needs to be appointed to manage the partnership – this might be the client or family office. As the GP typically has unlimited liability, this function will often be structured as a Special Purpose Vehicle (SPV).

The limited partners will sign ‘Adherence Agreements’ to specify how they will interact with the partnership.

In the case of a family Limited Partnership, the principal client may initially hold 100% of the interests in the Limited Partnership, and then periodically gift further interests to family members.

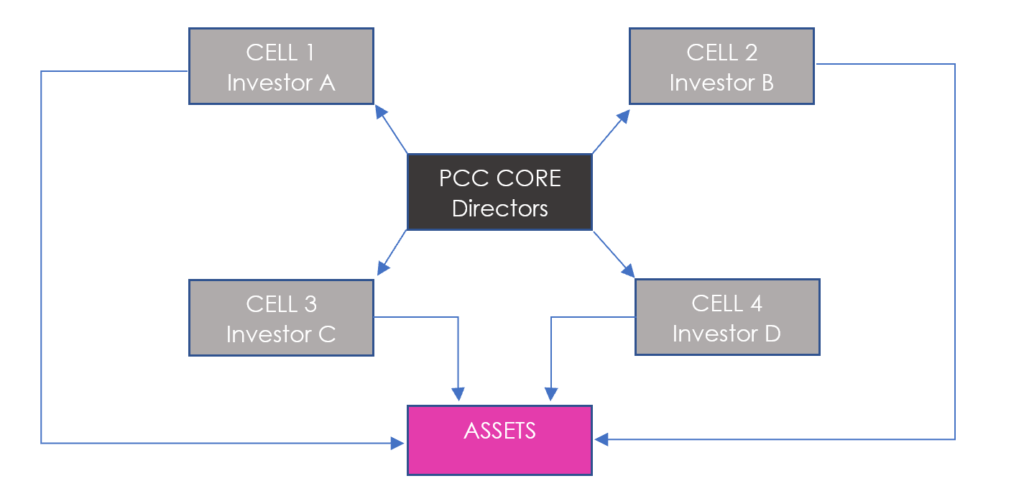

Protected Cell Company

A Protected Cell company (PCC) consists of one or more cells, each of which may be owned by separate clients. There is no comingling of assets and liabilities between the cells.

The cells are managed by the directors who can choose to contract out the administrative and accounting functions provided to each cell.

Costs are reduced, when compared to SPV vehicles or individual trusts, as overheads can be allocated to cells on a pro-rata basis.

Conclusion

Interest in PFs continue to grow as they offer an efficient tool for private wealth structuring.

Family members and groups of investors can benefit hugely from pooling their assets to maximise benefits. The ability to unitise specific assets, such as real estate, aircraft and artwork is also very useful.

The legal concept of a PF can be more straightforward for clients to understand, compared to a trust and/or a foundation, as the different investors hold specified units and will have agreed voting rights.

Additional Information

For additional information regarding Private Fund Structures in Guernsey please speak to Steven de Jersey or John Nelson at the Dixcart office in Guernsey: advice.guernsey@dixcart.com, or to your usual Dixcart contact.

Dixcart is licensed to provide fund administration services in Malta and in the Isle of Man.

We provide a comprehensive range of services in Malta including accounting and shareholder reporting, corporate secretarial services, fund administration, shareholder services and valuations.

The Benefits of Establishing a Fund in Malta

A key benefit in terms of using the jurisdiction of Malta for the organisation of a fund is the favourable tax regime. In addition, the fees for establishing a fund in Malta and for fund administration services are considerably lower than in a number of other jurisdictions.

Malta also has a comprehensive Double Tax Treaty network.

What are the Taxation Advantagesof Establishing a Fund in Malta?

Funds in Malta enjoy a number of specific tax advantages, including:

No stamp duty on the issue or transfer of shares.

No tax on the net asset value of the scheme.

No withholding tax on dividends paid to non-residents.

No taxation on capital gains on the sale of shares or units by non-residents.

No taxation on capital gains on the sale of shares or units by residents provided such shares/units are listed on the Malta Stock Exchange.

Non prescribed funds enjoy an important exemption, which applies to the income and gains of the fund.

A Self Managed Maltese UCITS Scheme and Dixcart and Fund Administration

A UCITS is one type of fund that can be organised in Malta and a self managed Maltese UCITS scheme can be established as an investment company.

The investment function can be delegated to a manager based in Malta or in another recognised jurisdiction. The administrator should preferably be based in Malta and the custodian or depository must be based in Malta. A Maltese UCITS can apply for listing on the Malta Stock Exchange.

The Dixcart office in Malta holds a fund licence and can therefore provide the appropriate fund administration services.

Additional Information

If you require any further information regarding the benefits of establishing a fund in Malta please speak to Sean Dowden at the Dixcart office in Malta: advice.malta@dixcart.com.

Sign up

To sign up to receive the latest Dixcart News, kindly visit our registration page.